- Case StudyHelp.com

- Sample Questions

Are you looking for Interpreting Financial & Accounting Information Assignment Questions? Our team of professional writers provides the top Financial Accounting Assignment Help for university students. Casestudyhelp.com covers a wide range of assignments, including dissertations, MBA, Case studies, etc., at a reasonable price, delivers AI-free content, and offers 24/7 live chat support.

Malayan Flour Mills Berhad – An Overview

Malayan Flour Mills Berhad is a Malaysia-based company, which is principally engaged in the business of milling and selling wheat flour, and trading in grain and other allied products. It is a Kuala Lumpur based company which was established in 1961 and listed on Bursa Malaysia in 1968.

The company operates, primarily, in two businesses: flour and poultry. The former involves milling and sales of wheat flour, trading in grains and other related products, whereas the latter segment involves manufacturing and sale of animal feeds, farming, processing and sale of poultry products. Flour and poultry make up roughly 68% and 32% of its revenue, respectively.

Malayan Flour Mills is the second largest flour miller in the country, behind Federal Flour Mills of the PPB Group. Its flour products are sold in both industrial and retail/household packs. Currently, the company has milling operations in Malaysia, Vietnam and Indonesia. The company is also the third largest broiler producer in Malaysia, behind Leong Hup. Its poultry product range consists of dressed chicken, marinated chicken and further processed products. The bulk of the chicken is sold for domestic consumption.

The company’s poultry farm practices closed house integration and is located in Manjung, Perak. In June 2017, the company added 7 fish feed production lines to its business. The newly set up aquatic feed mills can utilise the by-products from flour milling and poultry processing. The company also engages in hedging and trading of raw materials for flour and animal feeds.

Financial Statements of both corporate organisations Malayan Flour Mills Berhad

PPB Group Berhad – An overview

PPB Group Berhad is a Malaysian diversified conglomerate which engages in food production, agriculture, waste management, film distribution, property investment and development. PPB is also the single largest shareholder of Wilmar International, one of the leading palm oil producers and agribusiness companies in the world. The company was founded in 1968 as Perlis Plantations Berhad to cultivate and mill sugar cane in the state of Perlis. The company was listed in 1972 and since then has ventured into other industries. It exited the sugar business in 2009. Today, its main business is the supply of flour to downstream food producers.

PPB Group Berhad

| Question | Topic | % |

| 1(a) | Calculate 20 ratios mentioned in the study text under the following five categories for the two years in the financial statements for Malayan Flour Mills Berhad and PPB Group Berhad:

Profitability Ratios (5 ratios): (i) Return on Capital Employed (ii) Return on Shareholders’ Equity (iii) Operating Profit Margin (iv) Gross Profit Margin (v) Net Profit Margin

Asset Efficiency or Turnover Ratios (6 ratios): (i) Total Asset Turnover (ii) Non-current asset turnover (iii) Rate of inventories turnover (iv) Rate of inventories turnover (v) Rate of collection of trade receivables (vi) Rate of payment of trade payables

Liquidity or Solvency Ratios (2 ratios): (i) Current ratio (ii) Quick Ratio Gearing or Debt Ratios (4 ratios): (i) Equity gearing (ii) Total capital gearing (iii) Interest gearing (iv) Interest cover Investment or Market Value Ratios (3 ratios): (i) Earnings per share (ii) Price/Earnings (iii) Dividend payout |

36% |

| Note: Answers to ratio questions must follow the sequence in the lists presented in the question. Students must label the ratios according to the names given for each of them and the ratio figures derived from the respective formulas as either per cent, times, days, etc.

When the required information is not available in the provided financial statements, students may refer to the respective company’s annual reports. These reports can typically be accessed through the company’s official website. Students should also review the “Notes to the Financial Statements” as necessary, as these sections often contain more detailed disclosures and explanations relevant to the analysis. If some of the necessary information for a particular ratio is unavailable, the ratio may be left uncalculated. However, students must clearly state which specific information is lacking that prevents the calculation of the concerned ratio. |

||

| Marks for Q1(a) shall be based on correct calculation of the ratios. Formulas for the ratios as per the study text and given in the appendix to the assignment question must be shown and used in the calculation. 20 pairs of ratios are expected for each organisation. Each correct ratio would earn 0.45 marks. Correct labelling of the ratios is important. Accuracy of calculation according to the formula given and the resulting ratios would be relevant in the award of marks. Where the ratios produced have decimal places, they should

be limited to just two decimal places only. |

||

| 1(b) | Write a report, from an analyst point of view, comparing the financial performance and financial health of Malayan Flour Mills Berhad and PPB Group Berhad for the years 2024 and 2023. The assessment report should strictly cover four areas only and they are: (1) profitability, (2) liquidity, (3) efficiency, and (4) gearing.

As regards ratios, only eight sets of ratios should be selected for the comparison, and they are: Profitability: (1) Return on Capital Employed (2) Return on Shareholders’ Equity Liquidity: (1) Current Ratio (2) Quick Ratio Efficiency: (1) Total Asset Turnover Ratio (2)Non-current Asset Turnover Ratio Gearing: (1) Capital Gearing (2) Equity Gearing The discussion should follow the sequence set out in the question. Thus, general information such as revenue and assets can be portrayed first and compared to identify trends and size differential where appropriate. This can then be followed by discussion first of profitability, second liquidity, third efficiency and fourth gearing. Word Length: The report should be concise and not exceed 800 words. |

24% |

| 2(a) | According to Companies Act 2016, the directors of a company shall prepare for each financial year a report. The directors’ report prepared under section 252 may include a business review as set out in Part II of Fifth Schedule of the Act.

Required: Prepare a concise business review firstly for Malayan Flour Mills Berhad and secondly for PPB Group |

20% |

| Berhad, using information contained in their annual reports for FY2024 in respect of the following only:

(a) a fair review of the company’s business; (b) a description of the principal risks and uncertainties facing the company; (c) a basic analysis of the development and performance of the company’s business during the financial year. Extract from CA 2016 on Business Review: A business review’s requirements are set out in Part II of the Fifth Schedule of CA 2016:The business review may, to the extent necessary for an understanding of the development, performance or position of the company’s business, contain— (a) a fair review of the company’s business; (b) a description of the principal risks and uncertainties facing the company; (c) a balanced and comprehensive analysis of— (i) the development and performance of the company’s business during the financial year; (ii) the position of the company’s business at the end of that year, consistent with the size and complexity of the business; and (iii) the key performance indicators of the company; (d) information about— (i) environmental matters, including the impact of the company’s business on the environment; (ii) the company’s employees; and (iii) social and community issues. Word Length: The writeup should not exceed 500 words for each company’s business review. |

||

| (b) | “A rights issue could be an attractive source of long-term finance for a public listed company”. Explain “Rights Issue” and discuss the pros and cons of a rights issue as a way of raising long-term finance. Provide three examples of Malaysian listed companies (other than those in Q1) which have used this method anytime within the last five years. Give basic details of the rights issue carried out.

Word Length: The writeup in total for this question should not exceed 800 words. |

20% |

| Total | 100% |

- STANDARD RUBRIC

- INDIVIDUAL ASSIGNMENT

- 2: Understand how financial statements and reports are prepared and evaluate them to provide insightful interpretation.

| Performance levels | |||||

| No | Traits | Poor (1, 2, 3, 4) | Fair (5, 6) | Good (7, 8) | Excellent (9, 10) |

|

1 |

Understanding |

Did not demonstrate understanding of numerical concepts – very poor in using numerical concepts for problem solving. |

Demonstrated a fair degree of proficiency in solving problems using numerical reasoning. Did not have knowledge of multiple tools. |

Demonstrated a good degree of understanding in solving numerical problems. Had some knowledge of multiple tools. |

Demonstrated a high degree of understanding and reasoning in solving numerical problems. Had knowledge of multiple tools. |

|

2 |

Interpretation of data | Did not demonstrate the ability to interpret data – very poor in interpreting data. | Demonstrated a fair degree of data interpretation. | Demonstrated a good degree of data interpretation. | Demonstrated a high degree of accuracy in interpreting data. |

|

3 |

Analysis |

Did not demonstrate the ability to use quantitative analysis of data to firm judgement and conclusions – very limited ability to use quantitative analysis of data to draw

conclusions. |

Demonstrated a fair level of ability to use quantitative analysis of data and draw conclusions. |

Demonstrated a good ability to use quantitative analysis of data and draw meaningful conclusions. |

Used quantitative analysis of data for the basis of deep and thoughtful judgement, drawing insightful and carefully qualified

conclusions. |

|

4 |

Data Presentation |

Did not demonstrate the ability to present data – very poor in presenting data. | Demonstrated a fair degree of presenting data. | Demonstrated a good degree of data presentation. | Demonstrated a convincing way of presenting data in an interesting manner. |

|

5 |

Link theory to practice (Application) |

Did not demonstrate critical reflections that link theory to practice – very limited in reflection and very poor in linking

theory to practice. |

Demonstrated fair reflections and a moderate link between theory and practice. | Demonstrated a good level of reflection and a good link between theory and practice. | Demonstrated critical reflections that link theory to practice in a meaningful way. |

Appendix:

Financial Ratios extracted from the Study Text

| Profitability | |

| Return on capital employed (ROCE) or accounting rate of return

(ARR) |

(ℎ + × 100

+ ) |

| Return on shareholders’

equity |

( )

( ℎℎ′ ) |

| Operating profit

percentage |

× 100 |

| Gross profit percentage | × 100 |

| Net profit percentage | × 100 |

| Note: operating profit = profit before interest and taxation | |

| Efficiency | |

| Total asset turnover | |

| Non-current asset

turnover |

|

| Rate of inventories turnover (number of

times) |

|

| Rate of inventories

turnover (in days) |

× 365 |

| Rate of collection of trade

receivables (in days) |

× 365 |

| Rate of payment of trade

payables (in days) |

× 365

ℎ |

| Liquidity | |

| Current ratio | |

| Quick ratio | (ℎ ℎ + ) |

| Gearing | |

| Equity gearing | + ℎ

ℎ + |

| Total or capital gearing | + ℎ |

| Interest gearing | + |

| Interest cover | |

| Investment | |

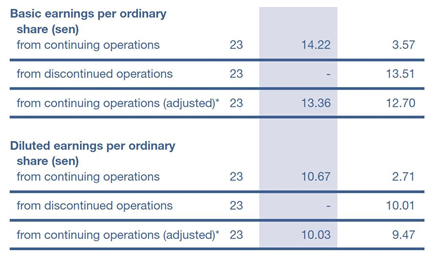

| Earnings per share | , ,

ℎ |

| Price/Earnings | ℎ |

| Dividend payout | ℎ

× 100 |

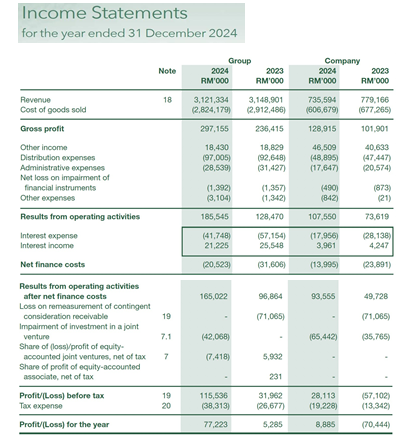

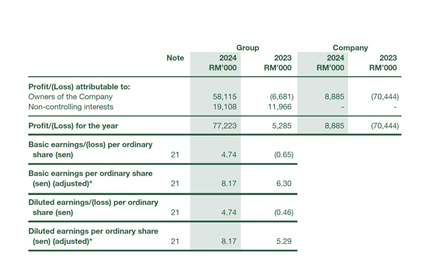

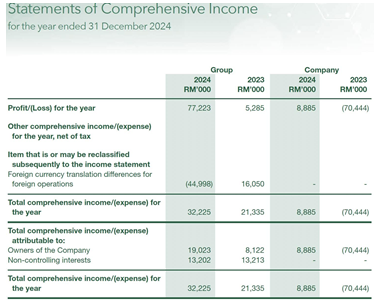

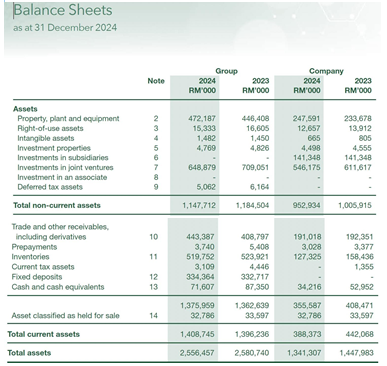

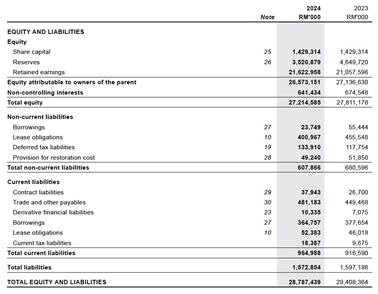

A. Malayan Flour Mills Berhad

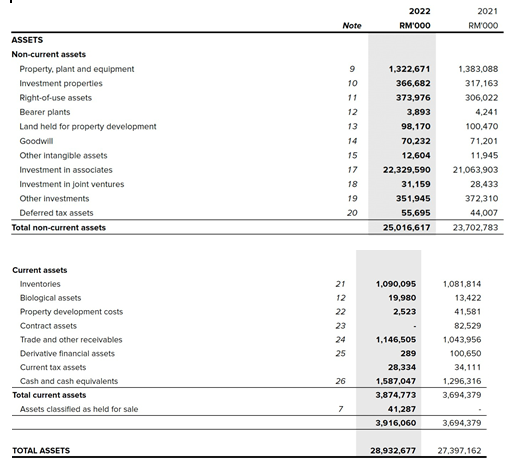

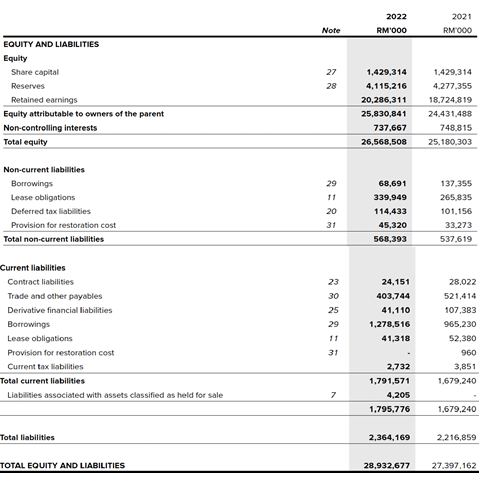

Statements of Financial Position As at 31 December

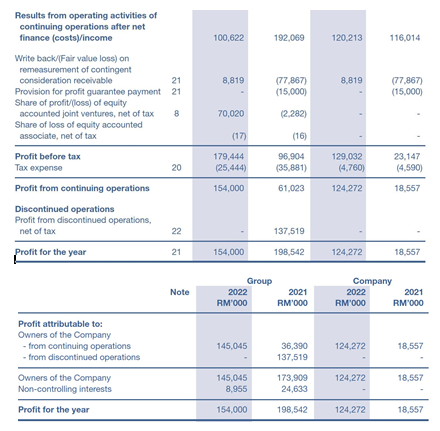

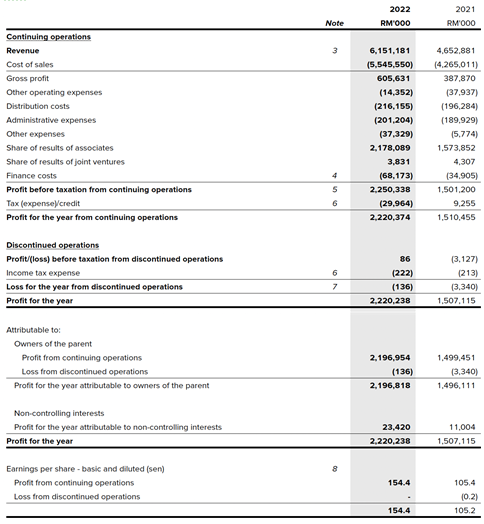

Statements of Profit or Loss

For the financial year ended 31 December

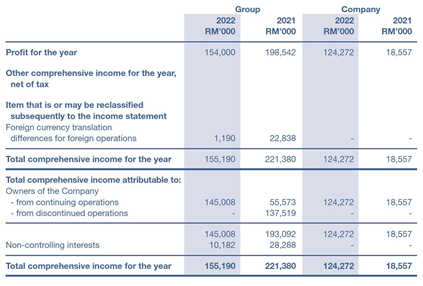

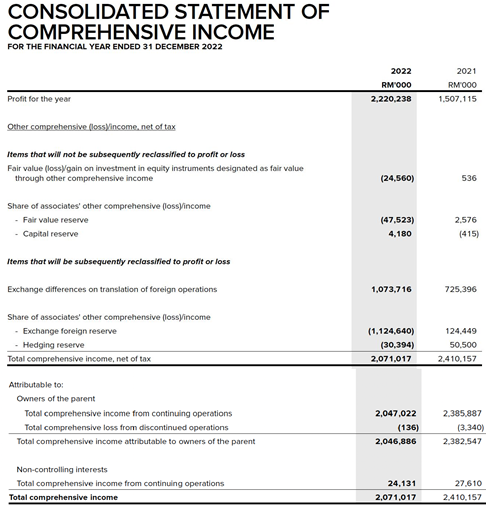

Statements of Comprehensive Income For the financial year ended 31 December

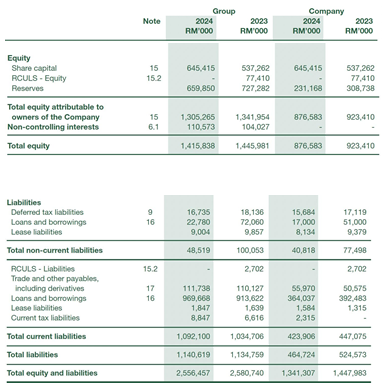

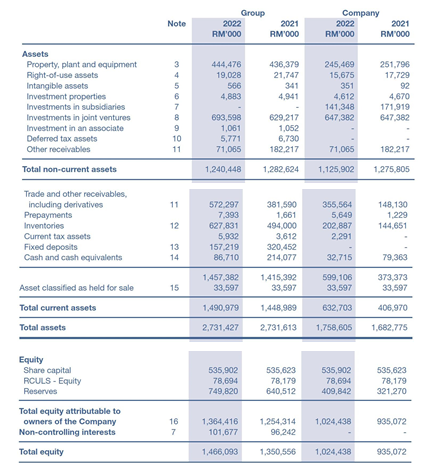

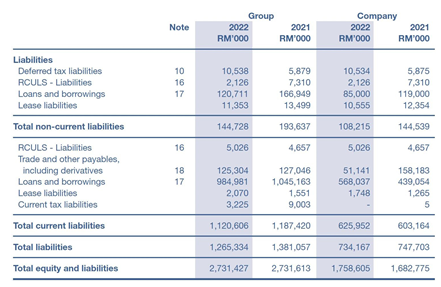

B. PPB Group Berhad

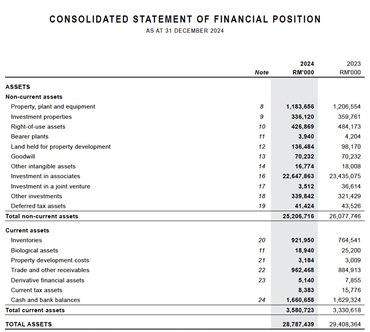

Consolidated Statements of Financial Position As at 31 December

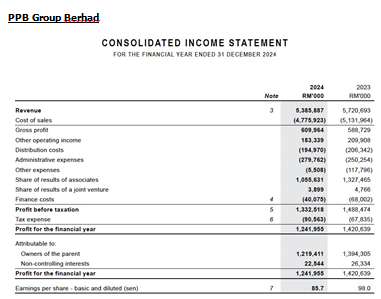

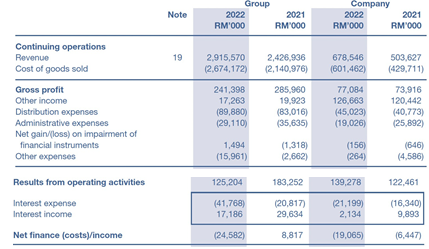

Consolidated Statement of Profit or Loss For the Year Ended 31 December

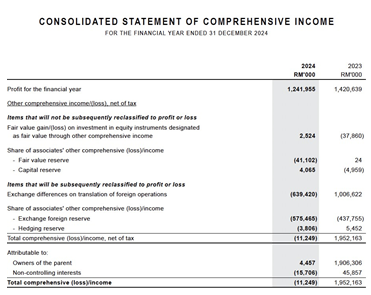

Consolidated Statements of Comprehensive Income For the Year Ended 31 December

For REF… Use:#getanswers2002761